70% of annual RFP lanes procured not materializing

FreightWaves on Tuesday interviewed Angela Acocella, postdoctoral researcher at Tilburg University and researcher with the MIT Center of Transportation and Logistics looking at the impact of ghost lanes on shipper and carrier networks. A ghost lane can be characterized as a lane that is awarded in a strategic bid or RFP but failed to materialize and no loads are tendered. During the discussion about the research, it was observed that between 65% and 80% of all lanes in an RFP can be ghost lanes depending on the bids occurrence in the freight cycle.

Acocella said that adding ghost lanes can negatively impact both shippers and carriers. Shippers that include all lanes in an RFP and fail to tender awarded lanes to carriers risk worsening carrier performance and higher pricing in the following year from their carrier networks. This stems from carriers paying additional costs from deadheads or attempting to solicit other customers to rebalance their internal freight networks after allocating capacity for a lane that failed to materialize.

The eventual impact of ghost lanes that do materialize can cause additional issues for shippers, with the research paper noting that “for the lanes that are characteristically ghost lanes but that do materialize, carrier rejection rates are high as are contract prices relative to spot market prices — in other words, shippers are overpaying anyway.”

Acocella added that factors like carrier and shipper reciprocity can also be negatively impacted if carriers are consistently awarded lanes that do not yield actual load tenders.

You can view the entire interview here

September preliminary Class 8 orders reach 2023 peak

ACT Research released preliminary September Class 8 orders on Wednesday, signaling a strong start to orders season now that orderbooks for 2024 are opening up. FreightWaves’ Alan Adler wrote ACT Research reported preliminary Class 8 net orders were 36,800 units, an increase of 67% month over month. Adler added rival analytics firm FTR Transportation Intelligence recorded orders at 31,200. Both numbers fell short of the record 53,700 orders in September 2022.

Kenny Vieth, ACT’s president and senior analyst said in the report, “One thing we did know was that nearly all the August-ending Class 8 backlog was scheduled for build in 2023, so strong orders are imperative for the industry to maintain current strong production rates very far into 2024.” Vieth cautioned, “While it is too early to infer much from September orders, data from the OEMs confirm the ‘season’ started on the right foot.”

Orderbooks can be subject to cancellations, which will be an important metric to watch in the coming months. Adler wrote, “Other orders are consistent with the beginning of the fall order season, when fleets book how many trucks they expect to need to replace older iron. Manufacturers allow order cancellations until they purchase materials to build the trucks. So, occupying build slots is ultimately a flexible hedge for the largest fleets.”

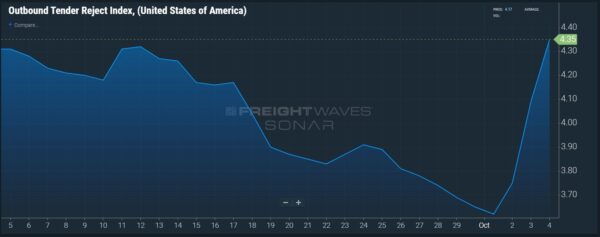

Market update: UAW strike potentially impacting outbound tender rejection rates

Nationwide outbound tender rejection rates are up 57 basis points week over week (w/w), from 3.78% on Sept. 27 to 4.35%, as carriers appear to adjust their networks from missing automotive volumes. Spikes in rejection rates in markets near plants would imply no inbound loads, thus reject the outbound.

Markets with automotive supply chain presence like Kansas City, Missouri, and Detroit are seeing a rise in outbound tender rejection rates. The Kansas City market, which includes Ford’s Claycomo assembly facility, saw rejection rates leap 449 bps w/w from 4.71% on Sept. 27 to 9.20%. Ford Assembly in Chicago feeds some shipments to Claycomo, which reported disruptions from the Chicago strike per the Detroit Free Press.

The Detroit market, which had sub-2% rejection rates for most of the month, rose 170 bps w/w from 1.7% to 3.4%. The last time rejection rates were this high was leading up to the Fourth of July holiday.

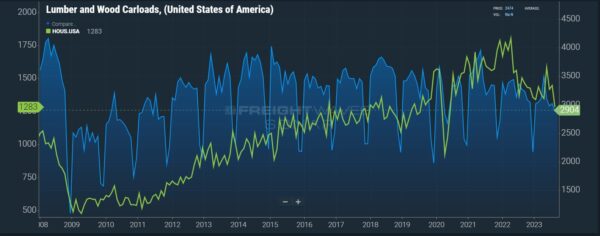

FreightWaves SONAR spotlight: Record mortgage rates fell lumber demand

Commentary courtesy of the Daily Watch, a newsletter for SONAR subscribers

Summary: The average rate on a 30-year fixed mortgage is bearing down on 8%, according to data from Bankrate. As of Wednesday, the rate had ballooned to 7.88% — a level not seen in more than 23 years. At the same time, the median sales price for an existing home in August was up 46% over August 2019, pricing the majority of would-be homebuyers out of the market. Given that, in its September meeting, the Federal Reserve both held interest rates at their highest target since early 2001 and adjusted the forecast to reflect a “higher for longer” rate strategy, the housing market is not expected to be hospitable to first-time buyers anytime soon.

Of course, this deterioration has had a sizable impact on demand for lumber. Prices for lumber have fallen $44 per 1,000 board feet, or 8.2%, over the past year. Rail traffic originated by lumber is at its lowest since mid-2011 (excepting seasonal distortions). This weakness in one commodity is spreading across commodity markets: Despite the extreme tightness of supply brought about by Saudi Arabia and other OPEC+ nations, domestic oil prices have tumbled 10% in just one week. The Flatbed Outbound Tender Reject Index (FOTRI), which benefits from activity in the construction and industrial sectors, is trending downward to its recent low of 5.04% — a reading itself FOTRI’s lowest since the initial stages of the pandemic.

The Routing Guide: Links from around the web

Judge rules TQL owes thousands of former employees overtime pay (FreightWaves)

Indiana trucking company’s bankruptcy tied to decline in coal demand (Trucking Dive)

How a fight over 2 jobs bankrupted union of 40,000 dockworkers (FreightWaves)

Freight turnaround might take until 2025: analysts (Trucking Dive)

XPO’s Jacobs on his next venture: Wait and see (FreightWaves)

Declines in transportation prices slow again in September (FreightWaves)

Like the content? Subscribe to the newsletter here.

NOVEMBER 7-9, 2023 • CHATTANOOGA, TN • IN-PERSON EVENT

The second annual F3: Future of Freight Festival will be held in Chattanooga, “The Scenic City,” this November. F3 combines innovation and entertainment — featuring live demos, industry experts discussing freight market trends for 2024, afternoon networking events, and Grammy Award-winning musicians performing in the evenings amidst the cool Appalachian fall weather.

[ad_2]

Source link