[ad_1]

In a freight market where the seemingly permanent prevailing question is, “Are we at the bottom, and if not, when is the bottom?,” Cass Freight Index data continued to report weak numbers but with some suggestion that a bottom may be near.

The headline on this month’s report is “Bouncing Along the Bottom.” “The volume downturn appears to be in the later innings, and after a long soft patch, we see the U.S. freight transportation industry on the cusp of a new cycle,” Tim Denoyer of ACT Research wrote in commentary accompanying the release of the June Cass data.

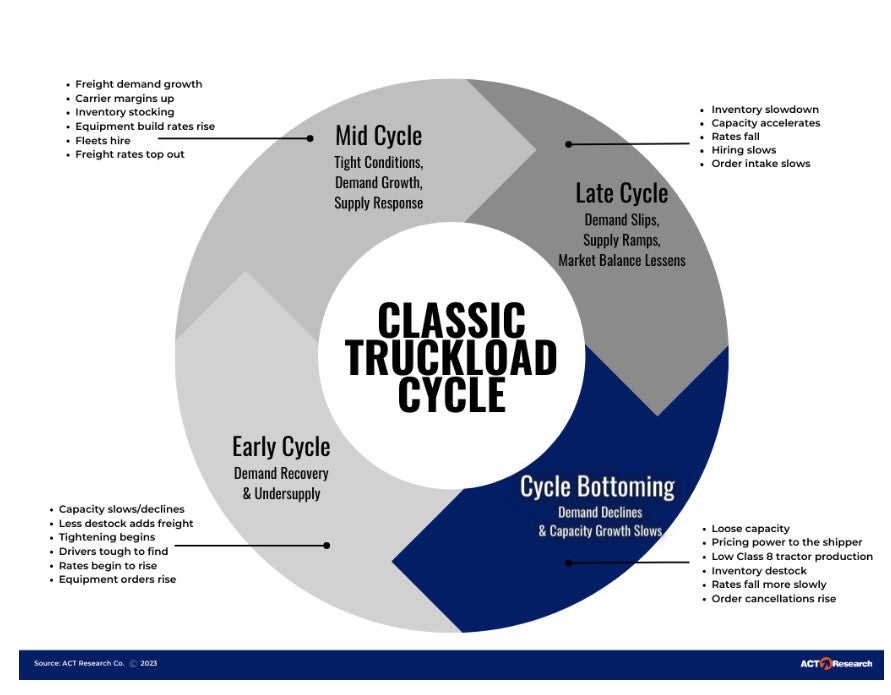

But the period that Denoyer said the freight market is moving into is what he calls “cycle bottoming.” In the graphic that accompanied the report, that cycle is marked by several features: loose capacity, pricing power to the shipper, low Class 8 tractor production, rates falling more slowly and order cancellations increasing. Overall, the biggest features highlighted on the “wheel” for cycle bottoming are that “demand declines and capacity growth slows.”

Denoyer did say that one aspect of cycle bottoming is missing in the current market: the lower level of equipment production. “As Class 8 build rates remain elevated, pressure remains on fleets to seat these tractors,” he writes.

In the main categories of the Cass Freight Index, the shipments component was down 1.6% month to month in June, which translated into a decline of 1.9% after seasonal adjustment of the data.

Compared to a year ago, the index was down 4.7%. That year-on-year decline was 5.6% for May, so the rate of annual decline was slower in June than in May. Seasonally adjusted, the shipments index is 12% less than the December 2021 cycle peak, according to Cass.

The report notes that the current “downcycle” is 18 months old, marked by that many year-on-year declines. The past three downcycles had durations of 21 to 28 months, Cass said.

The optimism over shipments is that while “declining real retail sales trends and ongoing stocking remain the primary headwinds to freight volumes, dynamics are shifting as real incomes improve and the worst of the destock is in the rearview,” Denoyer wrote.

The expenditures component of the Cass Index declined 2.6% sequentially from May and dropped 24.5% from a year ago.

Combining the data on declining shipments and the drop in expenditures led Cass to conclude that rates were down 1% in June from May.

Seasonally adjusted, the expenditures index was down 2.8% from May, with shipments declining 1.9% and rates falling 0.9%.

Fuel is in the expenditures index. The Cass Truckload Linehaul Index, which excludes fuel and so theoretically should be less volatile, was down 0.4% in June compared to May — a significantly smaller decline than the 2.6% month-to-month decline posted in May compared to April.

But the narrowing of the decline over the past two months masks the fact, according to Cass, that the 1.5% average decline over those two months is almost twice the 0.8% decline of the previous six months.

“As a broad truckload market indicator, this index includes both spot and contract freight,” Cass writes in the report. “With spot rates already down significantly, the larger contract market is likely to continue adjusting down.”

Beyond the 4.7% drop in the shipments index, the year-on-year declines remain substantial across the board among other Cass indices. The expenditures index is down 24.5%, inferred freight rates are down 20.9%, and the truckload linehaul index has declined 14.1%.

Morgan Stanley sees an upturn

The Cass report’s suggestion that the market has begun to bottom had some overlap with a Morgan Stanley report that projects that truck rates as measured by the Wall Street company will increase to $2.02 per mile in six months from the current $1.68, and will be $2.33 in 12 months.

Its Truckload Sentiment Survey (TLSS), according to a report from the team headed by Ravi Shanker, “overall reads more positive than [the most recent] update.”

“In a reversal from last update, current supply and rate sentiment switched from underperform to outperform this week, while current demand and 3-month forward supply sentiment switched to underperform,” the report said.

Among the survey’s respondents, expectations of trucking rates “remained steady, albeit still at the lowest levels in 2023 thus far after seeing a slight upwards inflection in mid-June.”

A large unknown: the fate of LTL carrier Yellow Corp. (NASDAQ: YELL) and a possible strike at UPS (NYSE: UPS). A closure of the former or a walkout at the latter “could … add significant upward pressure to rates, especially in the near-term,” the report said.

Cowen/AFS report also sees a reversal

Meanwhile, the TD Cowen/AFS Freight Index also saw a looming rebound in freight rates.

The Cowen/AFS index is expressed as a percentage over a January 2018 baseline. The projection is that in the third quarter, it will be 6.6% above the baseline, compared to 6.4% in the second quarter. Its peak was the first quarter of 2022, when it was 25.7% more than the baseline. In the second quarter of 2020, when the pandemic began, it was 40 basis points — 0.4% — less than the baseline.

If the third-quarter bounce does reach 6.6%, it will mark a reversal in a steady decline that went to 22.8% in the second quarter of last year after that 25.7% high water mark in the first quarter, and then slid sequentially for the next four quarters to 17%, 12.9% and 7.8% before the 6.4% of the second quarter of this year.

In a statement released alongside the data, AFS CEO Tom Nightingale said that while “risk of turmoil generates headlines, market conditions still favor shippers, even with truckload finally sending signals of price resilience.”

More articles by John Kingston

E2open execs tout year-over-year subscription, EBITDA growth

Truck transportation employment moves up and down in the same month

State of Freight for June: Few signs of upturn from historic lows

[ad_2]

Source link