[ad_1]

This week’s FreightWaves Supply Chain Pricing Power Index: 25 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 25 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 30 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Weak peak for ocean shipping

Maritime’s peak season — which typically ramps up in August and lasts throughout October — is expected by retailers and supply chain professionals to be weaker than it has been in previous years. While this tidbit is not necessarily surprising, it bodes poorly for truckload volumes headed into the fall.

The week before Independence Day is historically the last in which one could see elevated activity from shippers. Van volumes especially tend to be weaker during July, only rallying once the back-to-school season starts in mid-to-late August. But this year, the second quarter ended not with a bang but a whimper.

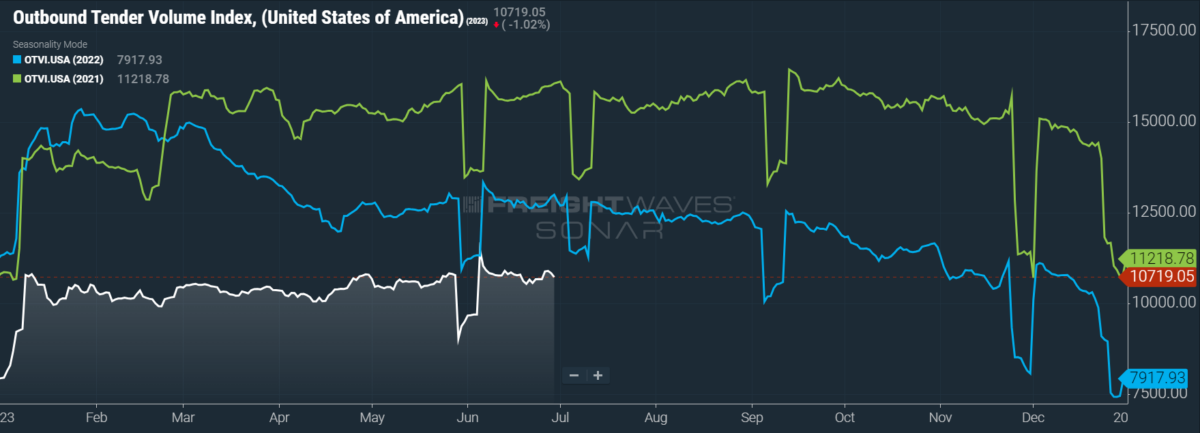

SONAR: OTVI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

This week, the Outbound Tender Volume Index (OTVI), which measures national freight demand by shippers’ requests for capacity, rose 1.54% on a week-over-week (w/w) basis. On a year-over-year (y/y) basis, OTVI is down 16.38%, though such y/y comparisons can be colored by significant shifts in tender rejections. OTVI, which includes both accepted and rejected tenders, can be inflated by an uptick in the Outbound Tender Reject Index (OTRI).

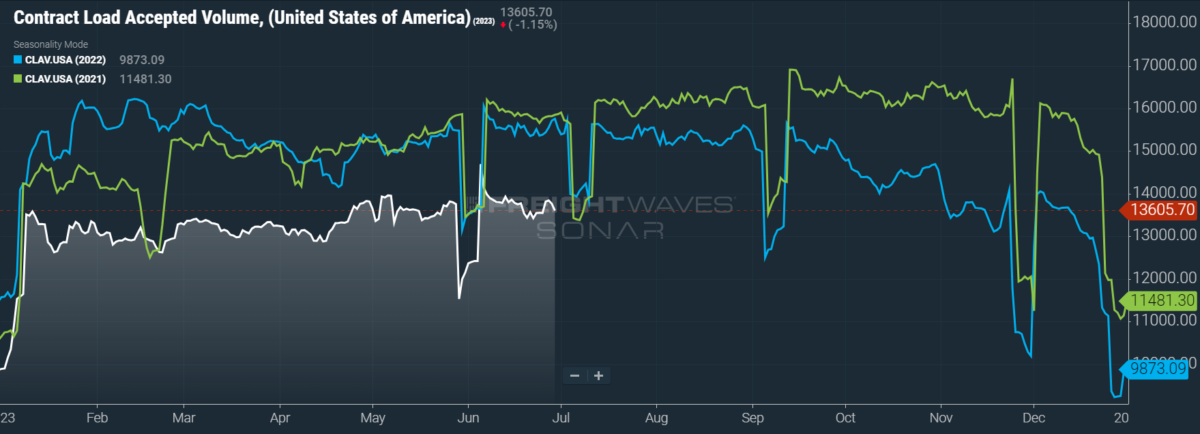

SONAR: CLAV.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Contract Load Accepted Volume (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a gain of 1.32% w/w as well as a fall of 12.75% y/y. This y/y difference confirms that actual cracks in freight demand — and not merely OTRI’s y/y decline — are driving OTVI lower.

Consumer spending during the summer is normally focused on bulky durable goods such as patio furniture, lawn equipment and outdoor grills. Increasingly, these goods have become affordable only through credit plans, especially the six-month “buy now, pay later” (BNPL) plan that has seen widespread growth. Yet consumer credit is already in a precarious state, even before factoring in October’s planned resumption of student loan repayments. Consequently, several BNPL firms — which had made their payment plans broadly available to grow market share — are now tightening their credit standards, fearing a potential wave of defaults.

Of course, consumer demand is not only falling in America but also on a global scale. This lack of demand has severely limited China’s post-COVID recovery, which was heavily staked on manufacturing and exports. But China’s manufacturing sector contracted for the third consecutive month in June, with the downturn driven by a lack of new orders and falling demand from abroad. In order to boost their flagging industrial economy, China’s central bank is among the few that has cut interest rates in the past month. Yet, at the time of writing, it is doubtful that China’s government will inject large amounts of credit into their economy, given that consumers and firms alike are more interested in paying down existing debt rather than making new investments.

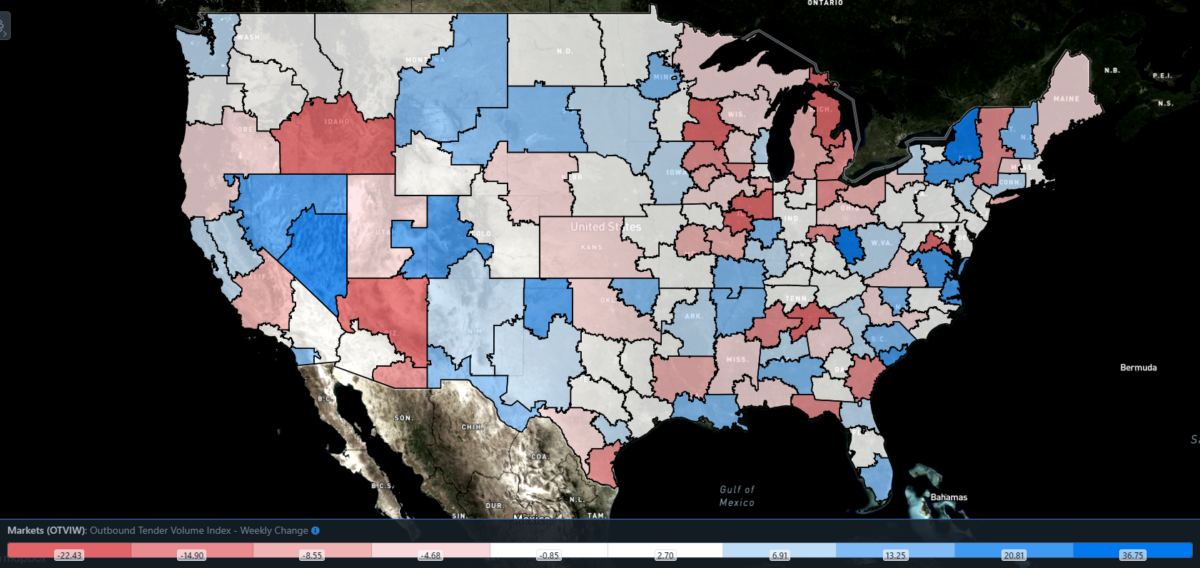

SONAR: Outbound Tender Volume Index – Weekly Change (OTVIW).

To learn more about FreightWaves SONAR, click here.

Of the 135 total markets, 79 reported weekly increases in tender volumes, though some key markets — like Atlanta — are falling behind.

Memphis, Tennessee, is a market that has risen to special prominence over the past month: Memphis is now the 12th-largest market by outbound tender volume, behind Detroit and Indianapolis but ahead of Columbus, Ohio, and Chicago. The market not only houses major logistics companies like FedEx but is also host to manufacturers of pulp and paper products, including the largest such firm in the world. This steady stream of volume, plus its relative proximity to other heavyweight markets like Dallas and Atlanta, has made Memphis one of the most attractive markets for carriers as of late.

By mode: Reefer volumes were something of a damp squib near the end of produce season, though Texas and especially Florida did end up with respectable outputs over the past couple of months. California, on the other hand, vastly underperformed in reefer volumes against the past three years. Given the late-winter flooding that swept the state, and that California law prohibits harvesting flooded farmland for fear of bacterial contaminants, such a weak performance was to be expected. So it is little surprise that the Reefer Outbound Tender Volume Index (ROTVI) is up only 1.3% w/w, slightly below the overall OTVI.

Van volumes, meanwhile, had a much more mediocre performance this week. The Van Outbound Tender Volume Index (VOTVI) was up a mere 0.34% w/w, with the lack of both imports and consumer demand for durable goods hurting van volumes. With the U.S. Supreme Court’s decision Friday to strike down the Biden administration’s student loan forgiveness proposal, consumer demand is likely to suffer this fall and during the winter holiday season.

Drivers take a break

Tender rejections have seen quite a rally over the past two weeks, though the gains are only significant relative to OTRI’s recent lows. On a market-level basis, tender rejections are still noticeably below a healthy average (5% to 7%). Some tightening is to be expected as drivers prepare for summer vacations around the Fourth of July, while others might conclude that they can save more money by parking their trucks than they would make — after operational expenses — by running loads. Inflation reports from the past few months have shown a devastating rise in costs for auto parts and maintenance, not to mention motor vehicle insurance.

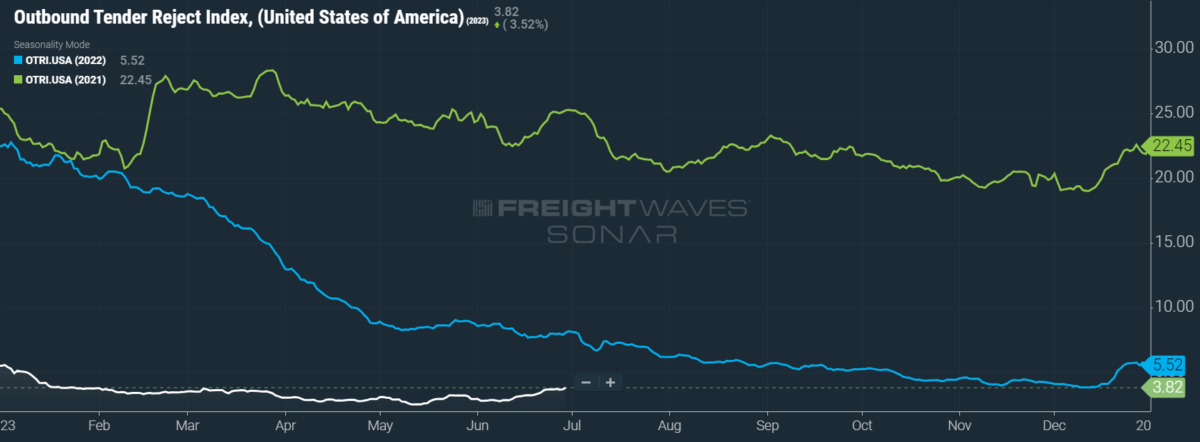

SONAR: OTRI.USA: 2023 (white), 2022 (blue) and 2021 (green)

To learn more about FreightWaves SONAR, click here.

Over the past week, OTRI, which measures relative capacity in the market, rose to 3.82%, a change of 20 basis points (bps) from the week prior. OTRI is now 427 bps below year-ago levels, with y/y comparisons becoming only more favorable as the year progresses.

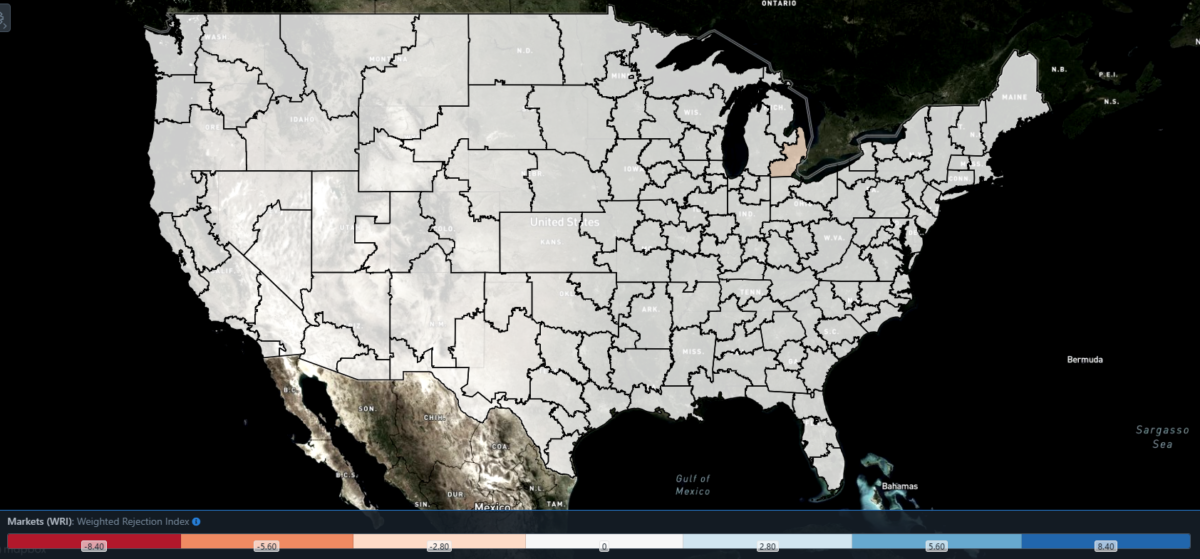

SONAR: WRI (color)

To learn more about FreightWaves SONAR, click here.

The map above shows the Weighted Rejection Index (WRI), the product of the Outbound Tender Reject Index — Weekly Change and Outbound Tender Market Share, as a way to prioritize rejection rate changes. As capacity is generally finding freight this week, no regions posted blue markets, which are usually the ones to focus on.

Of the 135 markets, 73 reported higher rejection rates over the past week, though 45 of those saw increases of only 100 or fewer bps.

To learn more about FreightWaves SONAR, click here.

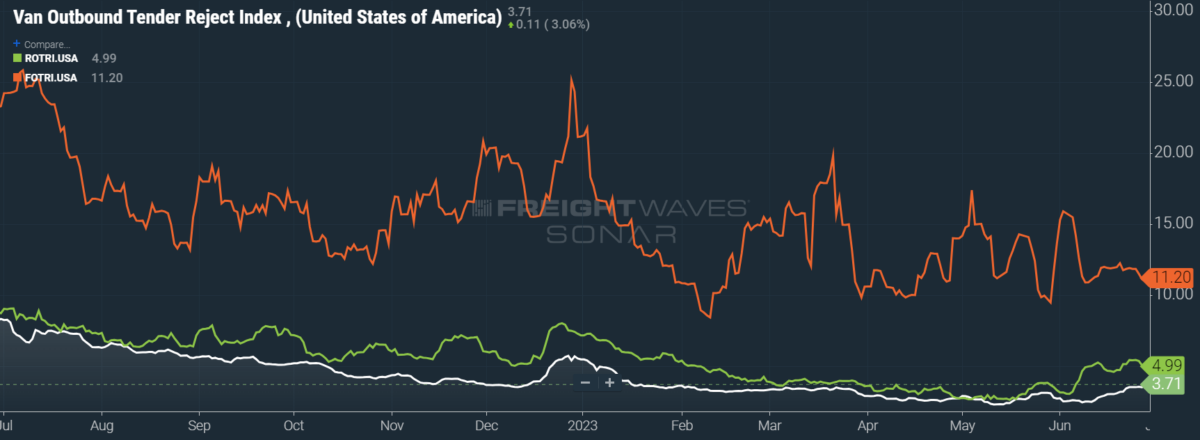

By mode: While its readings have resembled a roller-coaster track since the start of the year, the Flatbed Outbound Tender Reject Index (FOTRI) is finally evening out. FOTRI is useful as a proxy for the domestic industrial and construction sectors given its close relationship with the two. Unfortunately, June looks to be a middling month in both sectors, despite May’s surge in homebuilding activity. FOTRI is now at 11.2%, having fallen 65 bps w/w.

Reefer rejection rates have nearly doubled since May’s all-time low readings, but the Reefer Outbound Tender Reject Index (ROTRI) has come down off of its most recent highs. Despite a slight gain in reefer volumes, ROTRI slid 15 bps w/w to 4.99%. Van rejection rates, however, have been on a consistently upward trend since mid June, with the Van Outbound Tender Reject Index (VOTRI) having gained 27 bps w/w to reach 3.71%.

See spot (rates) sit

Spot rates, which had been one of the earliest warning signs of market deterioration back in 2022, are the greatest source of optimism that this cycle’s worst is behind us. That said, should carriers be celebrating spot rates’ performance right now? No, since they are stagnating far below inflation-adjusted rates from the previous downturn in 2019. Yet, if OTRI should maintain any momentum that it’s currently gathering, those gains will be a boon to carrier leverage in naming spot rates in the near future.

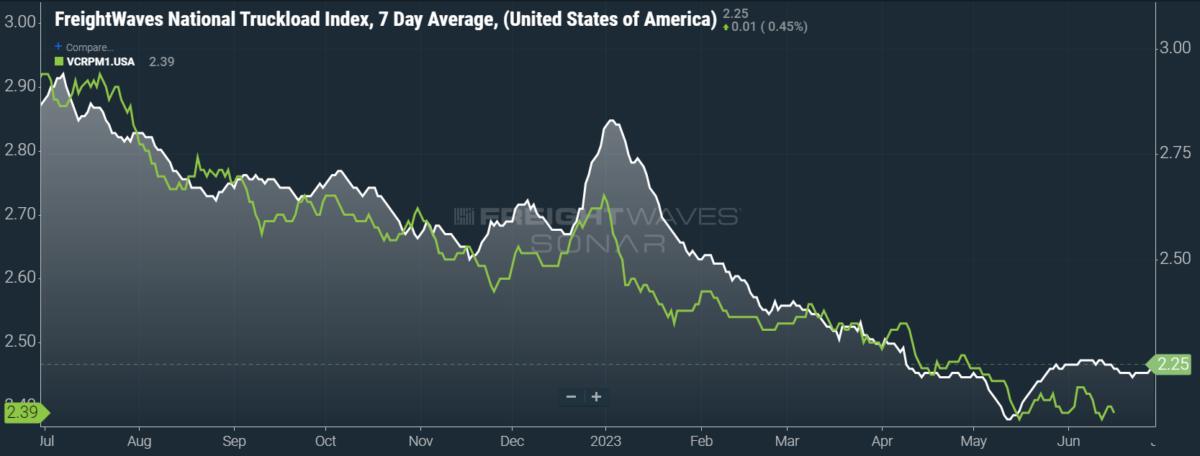

SONAR: National Truckload Index, 7-day average (white; right axis) and dry van contract rate (green; left axis).

To learn more about FreightWaves SONAR, click here.

This week, the National Truckload Index (NTI) — which includes fuel surcharges and other accessorials — rose 3 cents per mile to $2.25. Rising linehaul rates were the sole culprit behind this week’s gain, as the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — rose 3 cents per mile w/w to $1.65.

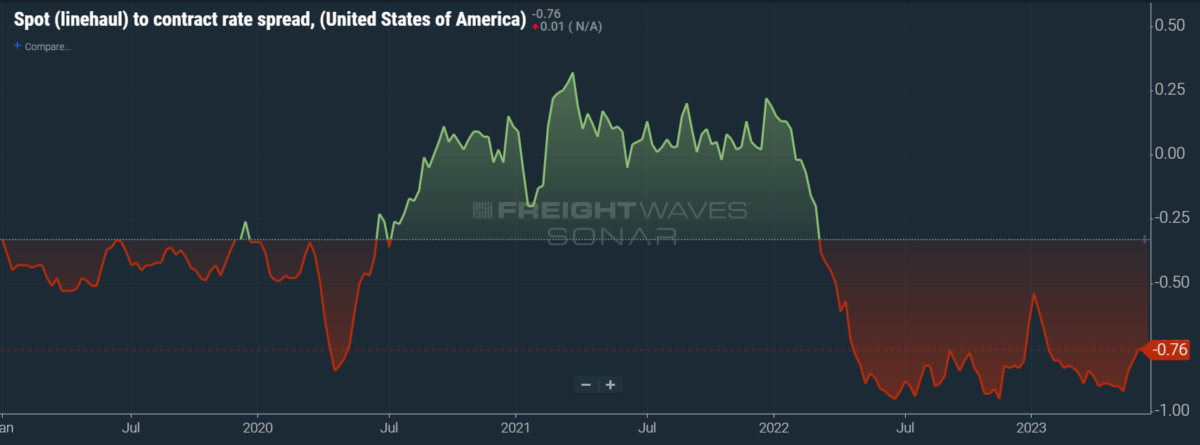

Contract rates have been on a downward trend since early April, albeit one that has had its brief reversals. By and large, contract rates are finally falling closer to a level that is to be expected after the significant depreciation of freight demand. I have, in previous columns, praised the foresight of shippers for not negotiating rates too low too quickly, as they would otherwise run much of their carrier base into bankruptcy — eventually sending rates much higher.

While no carrier is pleased with this present downturn, I would argue that contract rates are still coming down gently: The spread below between contract rates and linehaul spot rates is strong evidence of this slow comedown. So while contract rates — which exclude fuel surcharges and other accessorials like the NTIL, and which are reported on a two-week delay — have fallen 2 cents per mile w/w to $2.39, they could be much worse.

To learn more about FreightWaves SONAR, click here.

The chart above shows the spread between the NTIL and dry van contract rates, revealing the index has fallen to all-time lows in the data set, which dates to early 2019. Throughout that year, contract rates exceeded spot rates, leading to a record number of bankruptcies in the space. Once COVID-19 spread, spot rates reacted quickly, rising to record highs seemingly weekly, while contract rates slowly crept higher throughout 2021.

Despite this spread narrowing significantly early in the year, tightening by 20 cents per mile in January, it has since widened again. Since linehaul spot rates remain 76 cents below contract rates, there is still plenty of room for contract rates to decline — or for spot rates to rise — in the rest of the year.

To learn more about FreightWaves TRAC, click here.

The FreightWaves Trusted Rate Assessment Consortium (TRAC) spot rate from Los Angeles to Dallas, arguably one of the densest freight lanes in the country, continues to distance itself from April’s floor. Over the past week, the TRAC rate rose 3 cents per mile to $2.11 — still a distance from its year-to-date high of $2.39. The NTID, which has stabilized around $2.31, is handily outpacing rates from Los Angeles to Dallas.

To learn more about FreightWaves TRAC, click here.

On the East Coast, especially out of Atlanta, rates continue to rally, outpacing the NTID. The FreightWaves TRAC rate from Atlanta to Philadelphia rose 2 cents per mile w/w to $2.67. After a bull run that started at the end of April, these rates have been plateauing above the national average, which is making north-to-south lanes in the East far more attractive than West Coast alternatives.

For more information on FreightWaves’ research, please contact Michael Rudolph at [email protected] or Tony Mulvey at [email protected].

[ad_2]

Source link