[ad_1]

Weekly highlights

- Asia-US West Coast prices (FBX01 Weekly) decreased 5% to $1,778/FEU.

- Asia-US East Coast prices (FBX03 Weekly) fell 8% to $2,650/FEU.

- Asia-N. Europe prices (FBX11 Weekly) fell 34% to $996/FEU.

- Asia-Mediterranean prices (FBX13 Weekly) fell 4% to $1,751/FEU.

- China – N. America weekly prices increased 4% to $4.41/kg

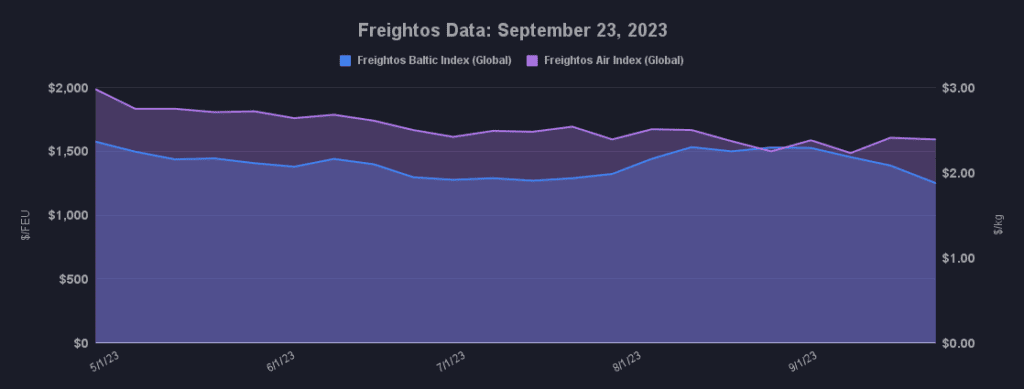

- China – N. Europe weekly prices increased 7% to $3.70/kg.

- N. Europe – N. America weekly prices increased 1% to $1.67/kg.

Dive deeper into freight data that matters

Stay in the know in the now with instant freight data reporting

Analysis

Last week, transpacific ocean rates continued their slide that started early this month. As this week’s rates have continued to decline, prices are now 17 – 20% lower than at the end of August. Sliding rates and reports of increased blanked sailings announced through October, likely signal that this year’s peak volumes are behind us.

Rates, and likely volumes too, are falling despite US consumer spending on goods remaining steady in August. A recent analysis suggests that some spending growth is on the types of goods, like video games, that don’t ship by ocean container – another factor in the relative disconnect between spending and freight.

But even with the rate declines of the last few weeks, prices to the West Coast remain well above 2019 levels, and East Coast rates are about even with 2019. Taken together with reports that utilization levels are over 90% to the West Coast, though closer to 80% to the East Coast, spot rates still above contract levels and likely above break-even mean carriers – for now – are managing transpac capacity successfully.

Carriers will seek to keep vessels full and prices from falling too much in the coming weeks through further blanked sailings and service suspensions – tasks that will only get more challenging as volumes ease and record levels of new capacity, about one vessel per day for the rest of the year, will continue to enter the global market.

Carriers are not having the same success on Asia – Europe lanes where rates crashed 34% last week to less than $1,000/FEU, an FBX record low for this lane. Despite significant blanked sailings and slow steaming, utilization levels are poor, pushing rates below contract levels, break even levels, and the $1,300/FEU mark that carriers were able to sustain from April through July. Carriers will blank even more capacity – about 20% announced so far – in October to try and push rates back up even as volumes likely decline on this lane too.

Despite transatlantic rates that are more than 40% lower than in 2019, and volumes likewise below 2019 levels (though they improved in July and August), this lane’s high share of capacity deployed via vessel-sharing agreements or by alliances is complicating carrier efforts to remove excess capacity and push rates up.

In air cargo, more forwarders are reporting signs of life for ex-Asia volumes, which is a good omen for hopes of an air peak this year. Freightos Air Index data show Asia – N. Europe rates of $3.70/kg have increased 27% since the end of August, and transpacific prices of $4.41/kg have climbed 10%.

Freight news travels faster than cargo

Get industry-leading insights in your inbox.

[ad_2]

Source link