[ad_1]

Freight shipments and expenditures improved from January to February but remained underwater compared to last year, Monday data from the Cass Freight Index showed.

Shipments increased 7.3% from January, up 2% when adjusted for normal seasonal trends, and were just 4.5% lower year over year (y/y). The y/y decline was the smallest in 10 months and 3.1 percentage points lower than January’s decline.

Severe winter weather in January as well as an extra day in February favorably impacted the comparisons.

“While seasonality remains soft in the near term and there are no more extra days on the calendar, underlying volumes have shown improvement,” the report said. “It’s been over two years since the first y/y decline of this freight recession, and with destocking playing out and goods consumption rising, we see this improvement as an encouraging sign that a recovery is beginning.”

The shipments index is forecast to increase 3% seasonally adjusted from the fourth to the first quarter. The data set is expected to turn positive on a y/y basis in May.

| February 2024 | y/y | 2-year | m/m | m/m (SA) |

| Shipments | -4.5% | -4.8% | 7.3% | 2.0% |

| Expenditures | -19.8% | -27.6% | 4.0% | 1.8% |

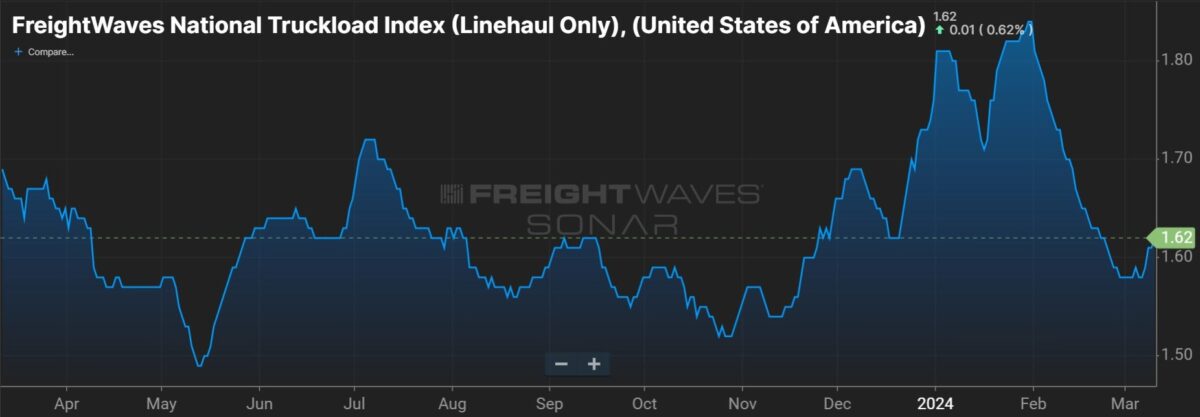

| TL Linehaul Index | -5.4% | -11.1% | 0.1% | NM |

Cass’ expenditures subindex, which measures all dollars spent on freight (including fuel surcharges and accessorial charges), was up 4% sequentially in February (1.8% higher seasonally adjusted). The index was off nearly 20% y/y, the smallest y/y decline since May.

The y/y change rates in the shipments and expenditures subindexes imply actual freight rates were down 3.1% from January to February and roughly flat when adjusting for seasonality. The subindex for implied rates hit a new cycle low during the month — the lowest reading since May 2021.

After declining 19% y/y last year, the expenditures subindex is expected to be down 14% in the first half of this year. The revised outlook is 200 basis points better than the forecast one month ago.

Cass’ truckload linehaul index, which excludes changes in fuel and accessorial charges, was up slightly from January but 5.4% lower y/y. The y/y decline was the smallest in more than a year as the index has moved sideways for the past eight months. Compared to two years ago, the index was off 11.1%.

The TL linehaul index captures changes in both spot and contract rates.

“While the freight cycle is certainly stabilizing with rates below sustainable levels in many cases and little room for further savings, we’re also seeing surprisingly strong new equipment orders for this point in the cycle,” the report said. However, the report noted “planning for upcoming emissions regulations is likely a key factor.”

“These capacity additions suggest the long bottom in the freight cycle may lengthen even further.”

Class 8 truck orders were up by low-double-digit percentages in both January and February.

Data used in the Cass indexes is derived from freight bills paid by Cass (NASDAQ: CASS), a provider of payment management solutions. Cass processes $44 billion in freight payables annually on behalf of customers.

[ad_2]

Source link